Uniswap LP Profitability Update

Uniswap LP Profitability Update

It's not sustainable

There are lots of people building on Defi—automated market makers, perpetual swaps, aggregators—and most think the decline in Defi volume is temporary, like a bear market. All users need, supposedly, is a better front-end, cheaper fees, or lower latency. While addressing these issues is helpful, they do not fix the fundamental problem: liquidity providers (LPs) lose money due to impermanent loss (IL).1 The standard solutions are not addressing this problem, which is an existential risk for Defi.

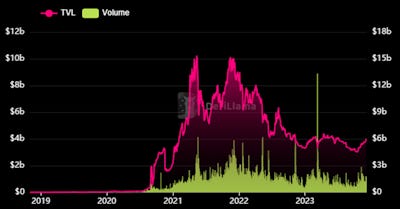

Here is the total Uniswap's Total Value Locked (TVL) and trading volume.

Uniswap Historical Activity (from defillama)

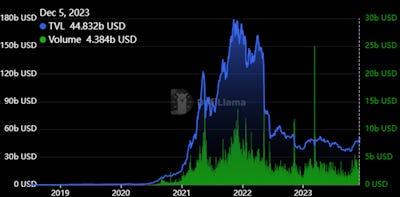

Other Dexs are not causing the prolonged Uniswap decline. Uniswap's decline is probably less than for any other Dex (note Luna caused the dramatic decline in May 2022).

Total Dex Historical Activity

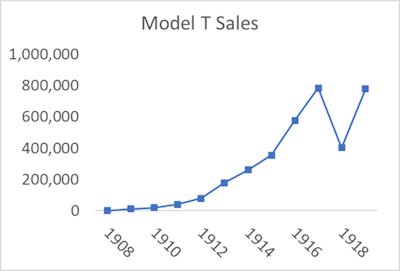

The initial growth is unrelenting in its first decade for transformational technologies like the transistor, planes, and automobiles. For example, here is a chart of Ford's sales of the first assembly-line car, the Model T, introduced in 2008. Note it rose exponentially for the first ten years, only declining amid WW1 (when over 50% of auto companies' production was focused on military goods). Growth resumed a year later and extended throughout the 1920s. So, outside of the massive shock of a World War, there were 21 years of constant growth.

Model T Sales

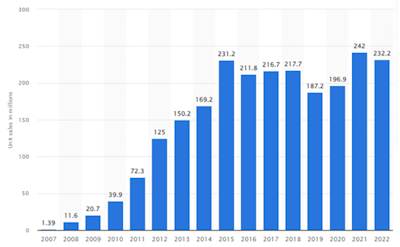

Another classic game-changing product was the smartphone, introduced by Apple in 2007. It saw nine years of exponential growth. By 2015, Apple's iPhone sales flattened, as new competitors arose.

iPhone Sales

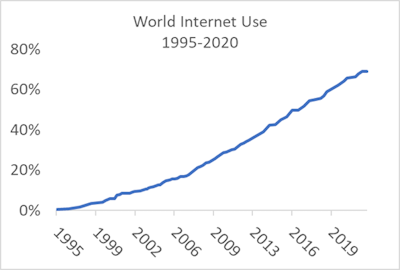

World Internet Use was also historic and has never experienced a significant one-year drop.

The usual pattern for transformational technology growth eventually flattens into the overall economic growth rate; however, initial growth is continual for at least a decade. No transformative technology had explosive growth in year one and then a 24-month retrenchment, as we see in Defi.

The cause of our Defi malaise is founded upon two main drivers. First, the token rewards were a great success, but ultimately temporary. SushiSwap started the Defi craze by giving out tokens to initial users, and early token holders made out big. When Uniswap decided to copy SushiSwap's token, it awarded many early Uniswap users thousands of dollars worth of Uni tokens. In 2021 several shitcoins vaulted into billion-dollar market caps—Shiba, Serum, Luna, Celsius, FTX, SafeMoon—with business models that were either logically absurd or built on vague delusions (FTT: you will buy bananas with it!). Crypto investors found that getting in early was more profitable than fundamental analysis.

Thus, when DyDx and Perp.fi gave out token rewards it created an ephemeral positive feedback loop: users deposit on the protocol to earn token rewards, outsiders look at TVL and volume and this pushes the equity token price up, making the rewards program not just attractive but profitable on its own, which encouraged more volume, which pushed up the token price, etc. Like Axie Infiniti, once the rewards stopped, the volume went back to a pathetic base rate.

PayPal got a big kick out of an initial giveaway where initial users got $20. That marketing gambit only worked because PayPal was doing something new and useful, creating a secure way to transact on the internet without typing in your credit card. PayPal's usage never dropped in its first years, let alone drop by 50%. Paying new customers to try your product is a legitimate business strategy, but it has become so common in crypto it no longer generates buzz, just misleading user data, especially as specialists have figured out how to game these rewards programs.

Rewards have recently returned. DyDx has a new rewards program to promote its new platform, and Arbitrum recently delegated $30MM to various dapps on their platform. It has provided a slight volume bump, but nothing like in 2021, as investors are not as credulous this time.

The second driver is that LPs continue to lose money. Why are they still there? Many are not convinced that impermanent loss is real because it's not a direct debit, just an opportunity cost. It goes away if one does not benchmark against one's initial LP deposit. After all, if the price of crypto goes up, an LP never loses money; he just makes less than otherwise.

The best way to see the flaw in this view is to consider a portfolio long a stock and short a call option, the covered call writing strategy. If the call option has a lower notional than the long stock position, the portfolio will always increase with the underlying, just with a less-than-linear function. If one does not benchmark against the original underlying stock position, the covered call writer would never lose money when the price rises, just as with an AMM LP.

The time value of an option has nothing to do with a risk premium; it is just the present value of convexity. If IL is not real, given the equivalence with a covered call position, call options should be priced at zero because those with covered call positions do not anticipate a real cost, and competition will push prices down to their cost in equilibrium. Call options are obviously not priced at zero. If you own a position with negative convexity, you need to be paid, as you effectively give someone an option.

Estimating Uniswap LP Losses

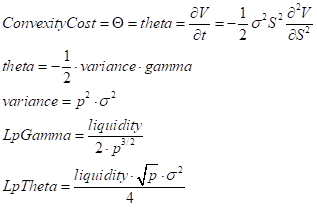

To estimate LP revenue, I simply multiplied the volume by the fee, translating everything into USD. To estimate the LP's convexity costs, I used two different metrics

In the first metric, I used the original Black-Scholes function for theta, which is the time decay in an option. Theta is a metric of the instantaneous loss rate from convexity, a function of the variance of the underlying and gamma. We can ignore interest rates, which are a distraction (at 5% annually, they don't significantly affect the results).

Black-Scholes theta applied to AMM LPs:

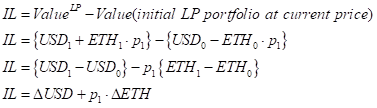

For the second metric, I used the realized LP ILs. One can think of the first method as the ex-ante in that it does not use the actual LP loss, only the loss implied by the assumption the LP is hedging a convex position. It is abstract, but it has been around for 50 years as a pillar of modern finance, and no one has refuted it; it's a credible metric. The second metric is more like looking ex-post at an option payout. The price of an option is the expected value of its payout, so over time, the payout on an option should approximate its price. The trick here is you need a large enough sample of data. If you look at one particular IL, say from mid-2021 to the present, you would see an IL of near zero, as the price of ETH was about $2200 at the start and finish. That does not mean the LP's convexity cost was zero; it just means that if a long-suffering LP kept their money in an AMM over that period, they got lucky.

LP IL metric

Using the pool math formulas for pool USD and ETH, we then have

Which rearranged becomes

One can use different volatility estimators, but they do not make a significant difference (e.g., apply the volatility of daily returns in a month for that month, use intraday data to estimate volatility each day). Data are in this spreadsheet.

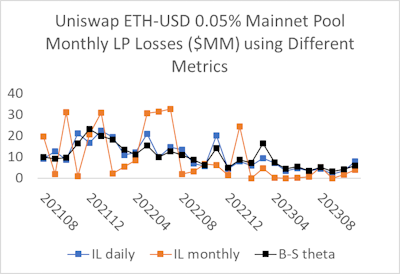

I estimated the IL using both monthly and daily data. To make them comparable, I summed the daily IL into a month.

The figure below shows that the average monthly convexity cost is the same for all approaches, about $10MM per month.

The IL metric using only month-end prices behaves like an out-of-the-money option, effectively zero several times but sometimes quite large. In practice, professional market makers hedge every day, as otherwise, their capital costs would be significantly greater, and over time the cost of convexity would not be different. Reducing capital costs by reducing one's tail risk is common sense.

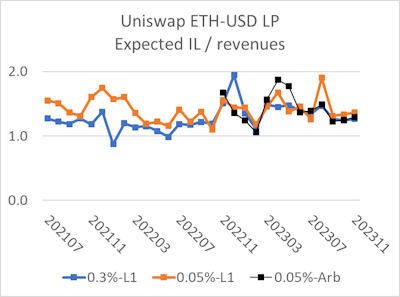

Below is the ratio of the convexity costs over monthly revenue for three major Uniswap pools. Note it is almost always greater than 1.0, representing an LP loss. It is not trending. The bottom line is that LP convexity costs are greater than revenue.

TL;DR

LPs are either ignorant or engaged in money laundering.2 Neither of these is the basis for a flourishing defi marketplace. AMMs need something new, soon.

Impermanent Loss is a specific outcome. Loss vs. Rebalancing, negative convexity, negative gamma, and theta are basically all the same thing and are the expected values of an IL.

I do not know of anyone specifically doing this, but a straightforward way to launder crypto is to make profits in one account by taking losses in another. So, a big stack of ETH from a hack or ICO can become kosher by throwing the tainted ETH into an LP position and then arbitraging that position. It would not make sense unless one was a substantial fraction of the LP pool. It could be the LPs are merely ignorant, but who knows.

Again good write up. I've been wrong for 35 years but my hope is a "single price auction" on a block chain. People just seem to like continuous markets though.

Ok so if LPs are getting this wrong, not realising they are selling call options, how does one take advantage of what are likely underpriced call options? Or is that just trading against the LP when the price moves?